Platform

Locations

Insights and Resources

News

About

Connect

XThis report provides market context for organizations evaluating Atlanta and the broader Fulton County area as a location for data center operations. It covers supply and demand dynamics, connectivity infrastructure, the power and regulatory environment, and tax considerations — drawing on current third-party research, local reporting, and publicly available market data.

Atlanta has undergone one of the most dramatic transformations of any data center market in the United States over the past three years. The metro led the country in net absorption in 2024 with 705.8 MW — surpassing Northern Virginia for the first time and representing a 222% increase in inventory that year alone. By early 2026, total installed capacity in the metro is estimated at approximately 1.82 GW, with projections pointing to continued rapid growth through the decade.

This growth is being driven by a convergence of factors: competitive power costs, Georgia’s historically favorable tax incentive structure, abundant land in the suburban corridor, and Atlanta’s deep fiber infrastructure. The city has evolved from a carrier-hotel-anchored colocation market — built around downtown institutions like 55 and 56 Marietta Street — into one of the most active hyperscale development corridors in the country. Fulton County alone has at least 464 MW of operating capacity and a further 396 MW planned or under construction.

The critical distinction for buyers: Atlanta’s growth story is predominantly a suburban, large-format, hyperscale story. The downtown core — centered on the Marietta Street carrier hotels — remains the city’s interconnection hub, offering something the suburban campuses cannot: deep carrier density, diverse fiber access, and the ecosystem that underpins colocation, peering, and latency-sensitive deployments.

Atlanta’s position as one of the Southeast’s premier connectivity hubs is rooted in its downtown carrier hotels. The Marietta Street corridor has served as the nexus of the region’s fiber ecosystem since the early internet era, and that foundation has only deepened as the market has grown. The buildings at 55 and 56 Marietta Street represent the most carrier-dense facilities in the Southeast, with dozens of carriers, internet exchanges, and network operators collocated within a single city block.

For enterprises and network operators, this concentration matters for several reasons: it minimizes the physical distance and cost of cross-connects between providers, enables peering arrangements within the same building, and provides access to the broadest set of last-mile and long-haul options in the region. The suburban campuses that have fueled Atlanta’s growth statistics are optimized for hyperscale power density — not for the carrier-diverse, low-latency interconnection that the downtown core provides.

Atlanta’s development pipeline is one of the most active in the country. Major projects announced or approved in the past six months include Blackstone-owned Link Logistics filing for a campus of up to 1.56 million sq ft outside the metro; Prologis’ Project Sail, a 900 MW, 4.34 million sq ft campus across nine buildings in Coweta County, approved in April 2026; and Microsoft confirming plans for multiple data center facilities near Atlanta as part of its East US 3 cloud region launching in 2027. Digital Realty closed a $3.25 billion hyperscale fund in March 2026 with Atlanta listed as one of its target markets.

In the downtown core, 55 Marietta Street and the adjacent 56 Marietta Street remain the market’s anchor interconnection facilities. Radius DC acquired 55 Marietta in 2025, establishing its Atlanta presence in the most carrier-dense building in the Southeast. With approximately 35% of the building’s 382,820 usable sq ft currently occupied, Radius DC offers one of the few remaining opportunities for significant scale in downtown Atlanta’s interconnection ecosystem.

Key takeaway: Pipeline supply is overwhelmingly hyperscale-oriented and suburban. Network-dense carrier hotel capacity in the urban core — the product relevant to enterprises, network operators, and carriers — is not being added at meaningful scale. Existing downtown inventory is the relevant supply for buyers with interconnection requirements.

Georgia Power is Atlanta’s primary electric utility, and it is in the midst of the largest grid expansion in the state’s history. In December 2025, Georgia regulators unanimously approved Georgia Power’s request for nearly 10,000 MW of new generation capacity — driven overwhelmingly by data center demand. The utility projects electricity demand will continue to grow by thousands of megawatts into the 2030s. To fund that expansion, Georgia Power expects to spend more than $52 billion on grid upgrades through 2030.

For buyers, Fulton County’s electricity rates are notably competitive: commercial and industrial rates run approximately 1.2% above the state average but 26.4% below the national average. Average time to power for new energy projects in Fulton County is approximately 3 years 4 months — better than both the Phoenix and national averages, though still a meaningful planning variable for new large-load deployments.

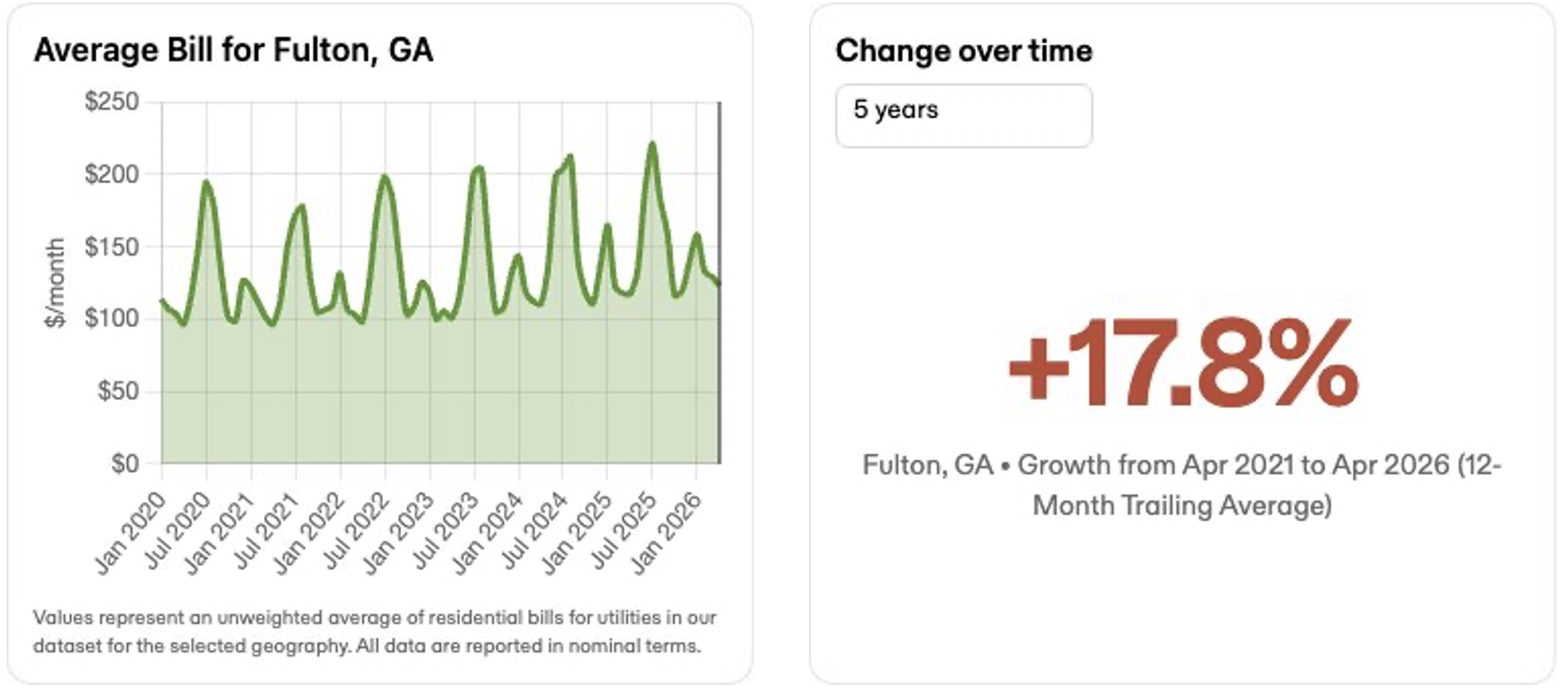

The charts below illustrate electricity cost trends for the Atlanta metro (Fulton County / Georgia Power service area). Average bills reflect seasonal peaks driven by summer cooling demand, with a +17.8% increase in the trailing 12-month average over the past five years — more moderate than Phoenix but a trend to monitor given the scale of planned grid investment.

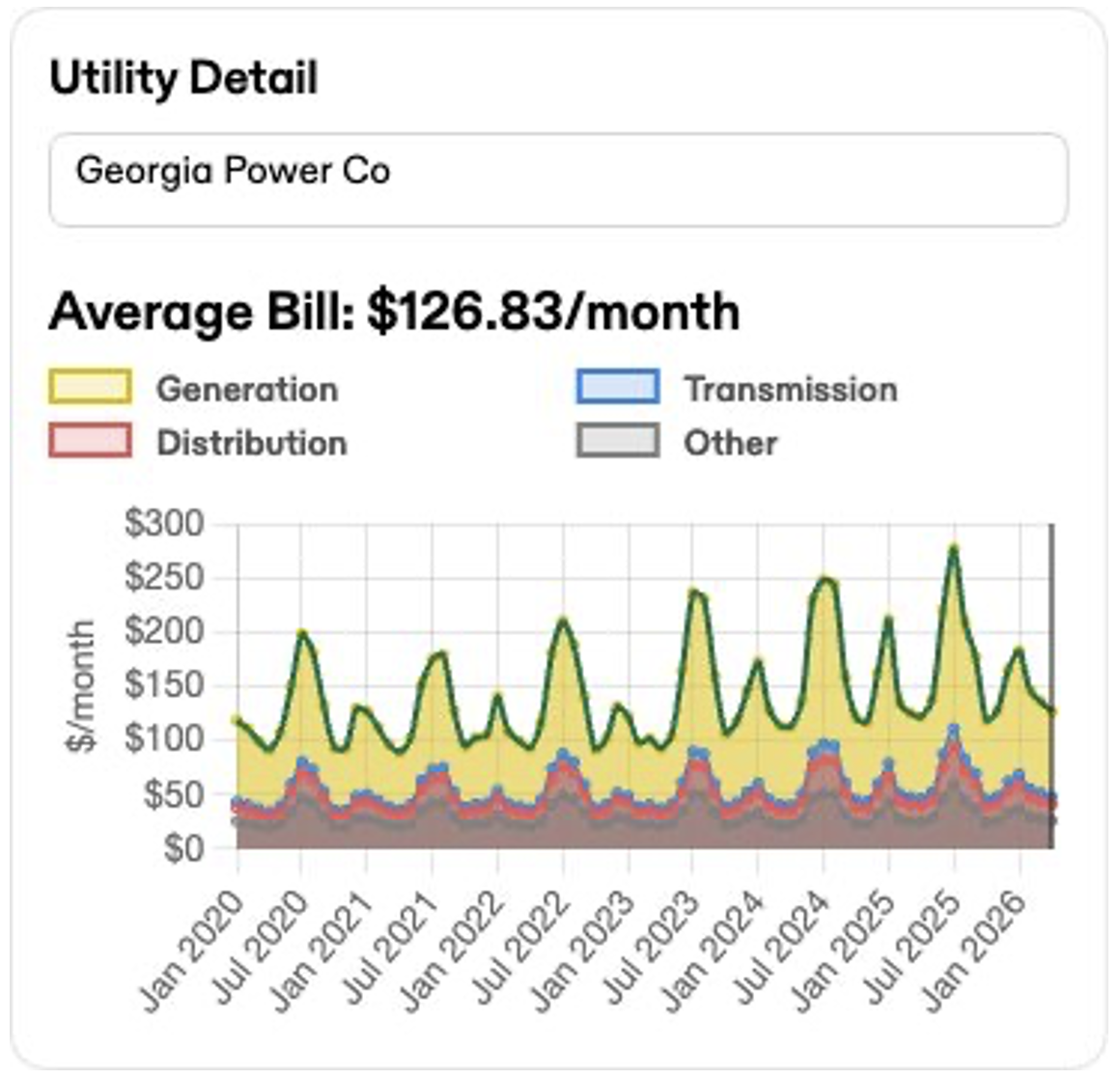

Georgia Power utility cost breakdown (generation, transmission, distribution):

Georgia has been one of the most aggressive states in the country in offering tax incentives for data center investment. The state’s primary vehicle is a sales and use tax exemption on data center equipment — applicable to qualifying owners, operators, and colocation tenants — which has driven an enormous influx of capital investment. A state audit estimated Georgia would forgo $2.5 billion in tax revenue in fiscal year 2026 alone as a result of the program. Georgia Power also offers data centers a reduced commercial electricity rate for an extended period before renegotiation.

The incentive structure is under political scrutiny, but the 2026 Georgia legislative session ended in April with the tax breaks left intact. Governor Kemp had previously vetoed a bill that would have revoked incentives for the largest facilities. A special legislative committee has been convened to study the issue, and the political environment around data center incentives in Georgia remains dynamic. Organizations building long-term financial models for Georgia deployments should monitor this closely.

For colocation tenants at qualifying facilities, the sales tax exemption on equipment purchases can represent a substantial operational cost advantage. Consult your tax and legal advisors to assess applicability to your specific deployment structure.

Atlanta and Fulton County have not enacted a data center moratorium at the city or county level, but the regulatory environment is evolving rapidly as community opposition grows. The risk report for Fulton County indicates a restrictive moratorium affecting data center projects, as well as at least one restrictive ordinance. A statewide moratorium bill was introduced in the 2026 legislative session but did not advance.

The opposition is most acute in suburban and exurban markets where large-format campuses are being developed — concerns over power lines, noise, land use, and water use are driving organized community resistance in Coweta, Henry, and other outer counties. In downtown Atlanta, the established carrier hotel environment operates in a fundamentally different context: existing buildings within the city’s urban core, with long-standing operating histories and minimal footprint expansion.

The Public Service Commission has enacted rules requiring data center operators to fund their own grid infrastructure costs rather than distributing them to residential ratepayers — a significant development that aligns the cost of growth more directly with those driving it.

Atlanta’s combination of connectivity heritage, cost structure, and market scale makes it one of the most compelling data center markets in the country:

Jaymie Scotto & Associates (JSA)

.png)