Platform

Locations

Insights and Resources

News

About

Connect

XThis report provides market context for organizations evaluating Indianapolis and the broader Marion/Hendricks County area as a location for data center operations. It covers Indianapolis’ rapid emergence as a major U.S. data center market, supply and demand dynamics, connectivity infrastructure, the power and regulatory environment, and tax incentives — drawing on current third-party research, local reporting, and publicly available market data.

Indianapolis has undergone a dramatic transformation from a regional colocation market into one of the most strategically significant data center corridors in the United States. The catalyst: Indiana’s combination of low power costs, generous and long-duration tax incentives, available land, central geography, and a low natural disaster risk profile has attracted some of the largest infrastructure investments ever made in a single U.S. state.

In February 2026, Meta broke ground on a $10 billion, 1 GW data center campus in Lebanon, Indiana — approximately 29 miles northwest of downtown Indianapolis in Boone County. Combined with Amazon’s $15 billion commitment for 2.4 GW of compute capacity in northern Indiana, Indiana is set to receive over $36.8 billion in data center investment from these two companies alone in the coming years.

Within Marion County and the immediate Indianapolis metro, the development pipeline is equally active. In early 2026, multiple large-scale projects have been approved or are in development: a $4 billion, 250 MW campus in Decatur Township; a $500 million, 72 MW facility in Martindale Brightwood; and a $2.2 billion, 410,000 sq ft campus at Thunderbird Commerce Center. The county currently has at least 12 MW of active data center capacity with 57 MW planned or under construction — representing roughly a 5x increase in local capacity.

For buyers, the market bifurcation matters: hyperscale campuses are concentrated in the suburban and exurban corridors where land and power are most available. Enterprise, edge, and carrier-neutral colocation in the Plainfield/Airport submarket serves a fundamentally different set of requirements — proximity to Indianapolis’ business base, connectivity to the metro’s fiber network, and operational flexibility that large-format campuses are not designed to offer.

Indianapolis benefits from its position at the geographic center of the United States — sitting at the intersection of multiple major fiber routes connecting the East Coast, Chicago, and the Southeast. The city’s connectivity infrastructure has developed alongside its manufacturing and logistics economy, with a diverse carrier ecosystem serving both the downtown core and the suburban industrial corridors.

The market’s fiber maturity is reflected in the scale of the investments being made: Meta’s Lebanon campus is specifically noted for its network building as part of the 15-building campus plan, and the broader hyperscale activity in the region is driving significant new fiber investment across the corridor. For enterprise and regional colocation buyers, the Plainfield/Airport submarket provides direct access to the fiber routes serving Indianapolis International Airport — one of the largest cargo airports in the United States by freight volume — and the industrial base that surrounds it.

Eli Lilly’s March 2026 launch of the LillyPod — the world’s first Nvidia DGX B300 SuperPOD AI supercomputer at its Indianapolis headquarters — illustrates the depth of enterprise AI infrastructure demand now present in the market. With 1,016 Nvidia Blackwell Ultra GPUs delivering over 9,000 petaflops of AI performance, it signals that Indianapolis enterprises are deploying serious compute locally, not just relying on cloud.

Indianapolis’ data center market is in an early but rapidly accelerating build-out phase. The existing colocation footprint in Marion County is modest — approximately 12 MW of operating capacity — reflecting the market’s historical role as a regional secondary market. That picture is changing quickly with the approval and groundbreaking of multiple large-format campuses in 2025 and 2026.

The pipeline skews heavily toward large-format, hyperscale-oriented product: the Decatur Township, Martindale Brightwood, and Thunderbird Commerce Center campuses are all wholesale or build-to-suit projects targeting hyperscale and large-enterprise tenants. Carrier-neutral, purpose-built colocation designed for enterprise workloads — the type that provides multi-tenant flexibility, carrier diversity, and operational proximity to the Indianapolis business community — is not represented in that pipeline. Radius DC’s Plainfield campus is specifically designed to fill that gap.

Key takeaway: Indianapolis is adding megawatts rapidly, but they are not the megawatts most enterprises need. Purpose-built multi-tenant colocation with carrier diversity, flexible deployment options, and proximity to the metro’s enterprise base is the underserved segment in this market — and the segment Radius DC is entering.

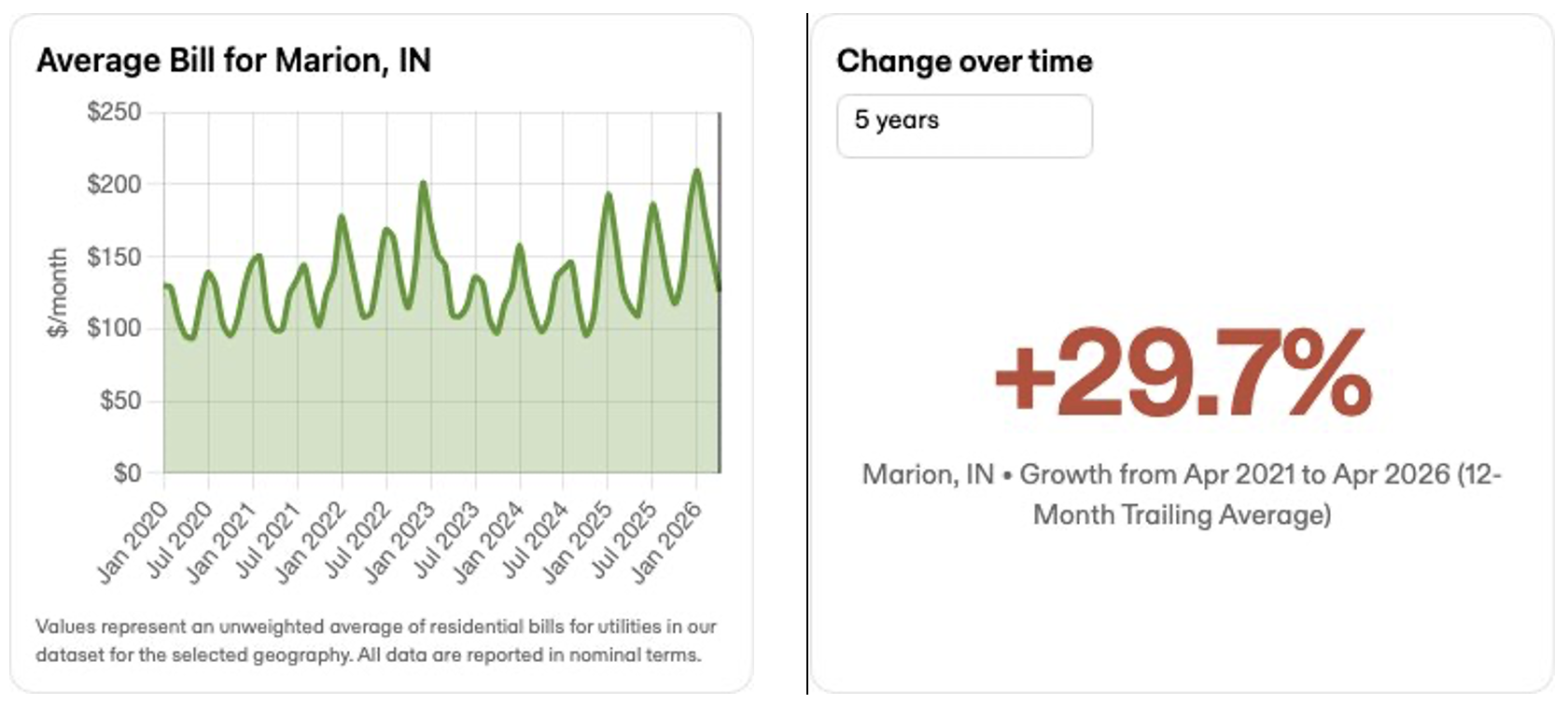

Duke Energy Indiana is the primary electric utility serving Indianapolis and the Plainfield/Hendricks County submarket. Marion County’s commercial electricity rates run approximately 13.3% below the Indiana state average and 22.8% below the national average — a structural cost advantage that is one of the primary drivers of the market’s attractiveness to data center operators. Average time to power for new energy projects in Marion County runs approximately 3 years 4 months, ahead of most other markets in this report.

Power demand pressure is emerging as a market variable. Indianapolis Power & Light (AES Indiana) filed a rate review request in mid-2025, citing increasing costs tied in part to data center load growth. The Indiana Utility Regulatory Commission is managing a growing volume of rate-related complaints, and the question of how utility grid expansion costs are allocated between data center operators and residential ratepayers is an active regulatory debate. Critically, Indiana has taken steps to address this: the legislature passed provisions requiring data centers to pay their full cost of energy service, and operators have committed to covering their own power infrastructure costs.

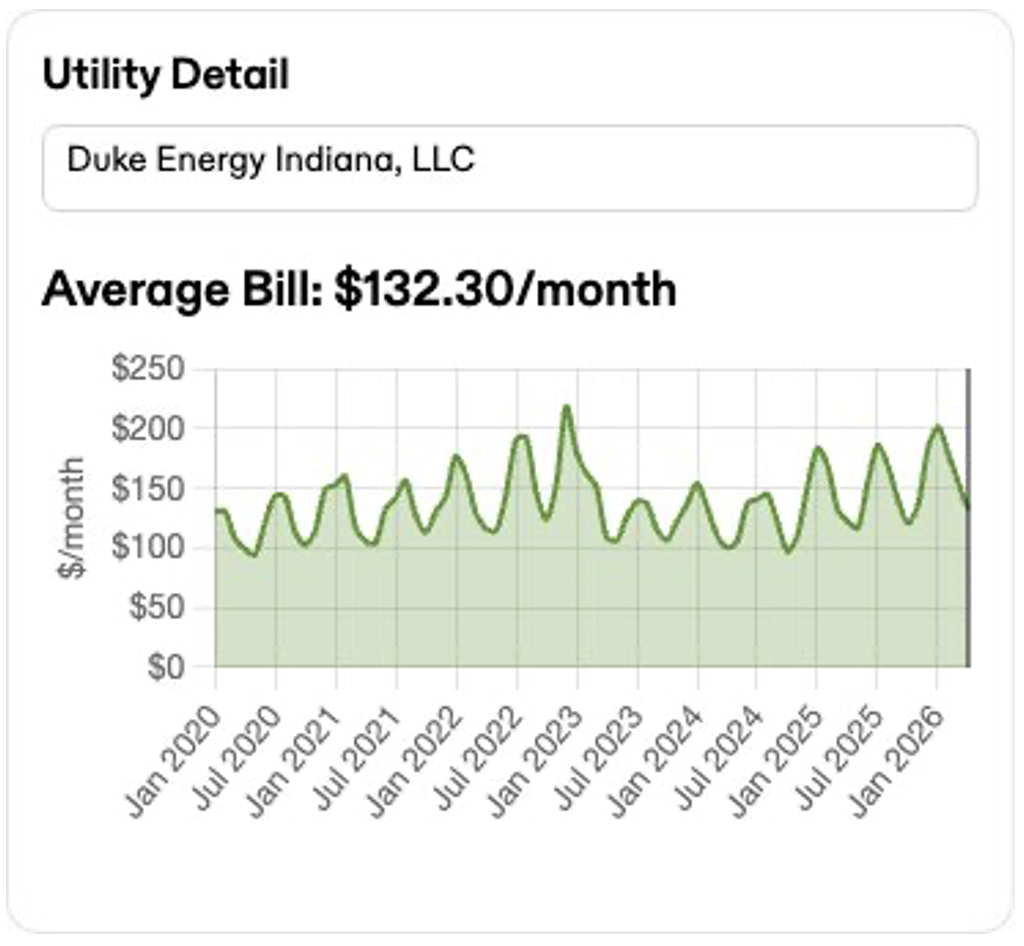

The charts below illustrate electricity cost trends for Marion County (Duke Energy Indiana service area). Average bills have risen +29.7% over the five years ending April 2026, driven by both increased demand and seasonal peaks. The Duke Energy utility detail shows a balanced generation/distribution cost structure with moderate seasonality compared to sunbelt markets.

Duke Energy Indiana utility cost breakdown (generation, transmission, distribution):

Indiana offers one of the most comprehensive data center tax incentive programs in the United States. The 2019 legislation — championed by the state’s utility committee chair — provides sales tax exemptions on both equipment purchases and energy costs, with exemption periods of up to 50 years. Local governments can additionally provide property tax abatements, and the Indiana Economic Development Corporation (IEDC) can offer further credits and grants for job creation and capital investment.

The program has attracted landmark commitments: Google received a 35-year term sales tax exemption (extendable to 50 years based on investment milestones) for its Indiana campus. The total fiscal cost of these incentives is substantial — analysis suggests Indiana data centers could cost the state up to $2.2 billion in tax breaks — which has generated legislative debate but, as of May 2026, the incentive framework remains intact. Governor Braun has been supportive of the program, attending Meta’s Lebanon groundbreaking in February 2026.

For colocation tenants, Indiana’s equipment and energy sales tax exemptions can represent a significant operational cost reduction for qualifying deployments. The extended duration of the exemptions — up to 50 years — is particularly valuable for organizations planning long-term infrastructure commitments. Consult your tax and legal advisors to assess applicability to your specific structure.

Indianapolis has no statewide data center moratorium, and Marion County has not enacted a restrictive ordinance or moratorium of the type seen in Denver or Atlanta’s suburbs. The risk report for Marion County shows no restrictive ordinances or moratoriums at the county level — a positive signal for operational certainty. However, community opposition to specific greenfield development projects within Indianapolis city limits has been significant and is the market’s most consequential near-term variable.

Opposition has been organized and, in one notable instance in April 2026, has escalated beyond protests: a city councilor’s home was shot multiple times with a ‘No Data Centers’ sign left at the scene — an extreme incident that underscores the intensity of community feeling around certain proposed projects. Opposition has been most concentrated around projects proposed for residential-adjacent or agricultural land in neighborhoods like Martindale Brightwood, Franklin Township, and Decatur Township. Projects withdrawn after public outcry include proposals in Pike Township and Franklin Township.

The critical distinction for buyers: the opposition is project-specific and location-specific, concentrated around large-format greenfield development in community-adjacent areas. Established industrial submarkets — particularly the Plainfield/Airport corridor in Hendricks County — carry a fundamentally different community and regulatory profile. Hendricks County has not been the site of organized data center opposition, and the Plainfield industrial corridor’s existing character is compatible with data center use.

Indianapolis’ emergence as a major data center market reflects a convergence of durable structural advantages:

Jaymie Scotto & Associates (JSA)

.png)