Platform

Locations

Insights and Resources

News

About

Connect

XThis report provides market context for organizations evaluating Nashville and the broader Davidson County area as a location for data center operations. It covers Nashville’s emergence as one of the Southeast’s most active emerging data center markets, supply and demand dynamics, connectivity infrastructure, the power environment, and the regulatory landscape — drawing on current third-party research, local reporting, and publicly available market data.

Nashville is classified by Cushman & Wakefield as an “emerging market” for data centers — a designation that accurately captures where the city is in its trajectory: past the early adopter phase, growing rapidly, and not yet saturated. The greater Nashville area had 27 data centers as of late 2025, with 25+ active in Davidson County and the surrounding metro. Nashville is the largest data center market in Tennessee, anchored by Meta’s Gallatin campus — a 12-facility, 900-acre development consuming up to 300 MW and representing one of the largest hyperscale deployments in the Southeast.

What’s driving Nashville’s emergence is a convergence of factors that distinguishes it from other ‘emerging’ markets: a rapidly expanding corporate and technology base anchored by Oracle’s planned world headquarters on the Cumberland River East Bank; TVA’s large and relatively stable power ecosystem; a business-friendly regulatory environment with no data center moratoriums; and a central Southeast geography that places Nashville within easy reach of Atlanta, Indianapolis, Charlotte, and St. Louis. The city is also one of the fastest-growing metros in the United States by population, which drives sustained enterprise demand for local digital infrastructure independent of hyperscale activity.

The market bifurcation familiar from Atlanta and Indianapolis applies here too: hyperscale campuses are concentrated in the Gallatin/Sumner County corridor, while enterprise colocation serving Nashville’s business community is anchored in Davidson County. These are different products serving different buyers.

Nashville sits at a natural crossroads for fiber infrastructure serving the Southeast. The city lies on major fiber routes connecting Atlanta to the south, Indianapolis and Chicago to the north, Memphis and the Mississippi Valley to the west, and Charlotte and the East Coast to the east. This geographic centrality has attracted a diverse carrier ecosystem that serves both the downtown core and the newer suburban industrial corridors.

The downtown carrier hotel ecosystem — anchored by the 147 Fourth Avenue facility — has historically been Nashville’s primary interconnection hub, with 16 carriers and the region’s broadest connectivity options accessible from a single building. That facility was acquired by HyscaleIX (a Novacap/H5 joint venture) in February 2026 as part of a strategy to build a North American carrier hotel portfolio — a signal that institutional investors see long-term value in Nashville’s network density.

The Trinity Hills corridor — where Radius DC’s Nashville I campus is located — provides access to the long-haul fiber routes serving Nashville’s northeast industrial and logistics base, with direct proximity to the NES grid infrastructure and the carrier options that define the facility’s connectivity offering.

Nashville’s data center market is served by a mix of legacy carrier hotel operators in the downtown core and newer purpose-built colocation facilities in suburban corridors. Established operators include Flexential (three facilities in the Brentwood/Franklin/Cool Springs corridor), Evoque (a 100 MW campus in Gallatin), and the carrier hotel at 147 Fourth Avenue now under HyscaleIX management.

New supply being added to the market in 2025–26 is notable for its variety. Radius DC’s Nashville I — the largest and newest colocation facility in Nashville proper — opened in 2026 and is now fully leased, reflecting the unmet demand in the market. At the institutional scale, Fisk University unveiled a $1 billion campus master plan in May 2026 that includes a 30 MW data center shell to be operated by a partner — an unconventional but notable signal of the depth of interest in Nashville’s data center market from unexpected directions.

Davidson County currently has at least 3 MW of active data center capacity with 12 MW planned or under construction — a market that by primary market standards is small, but one where purpose-built, carrier-neutral colocation in the urban core has been genuinely undersupplied. Nashville I is the most significant new addition to that segment in the market’s history.

Key takeaway: Nashville’s colocation market is not large, but it is growing and genuinely undersupplied at the enterprise end. The pipeline of new supply — outside of Meta’s hyperscale campus — is modest relative to demand, which is why Nashville I was fully leased at opening. Organizations evaluating Nashville should connect with Radius DC early to discuss waitlist options.

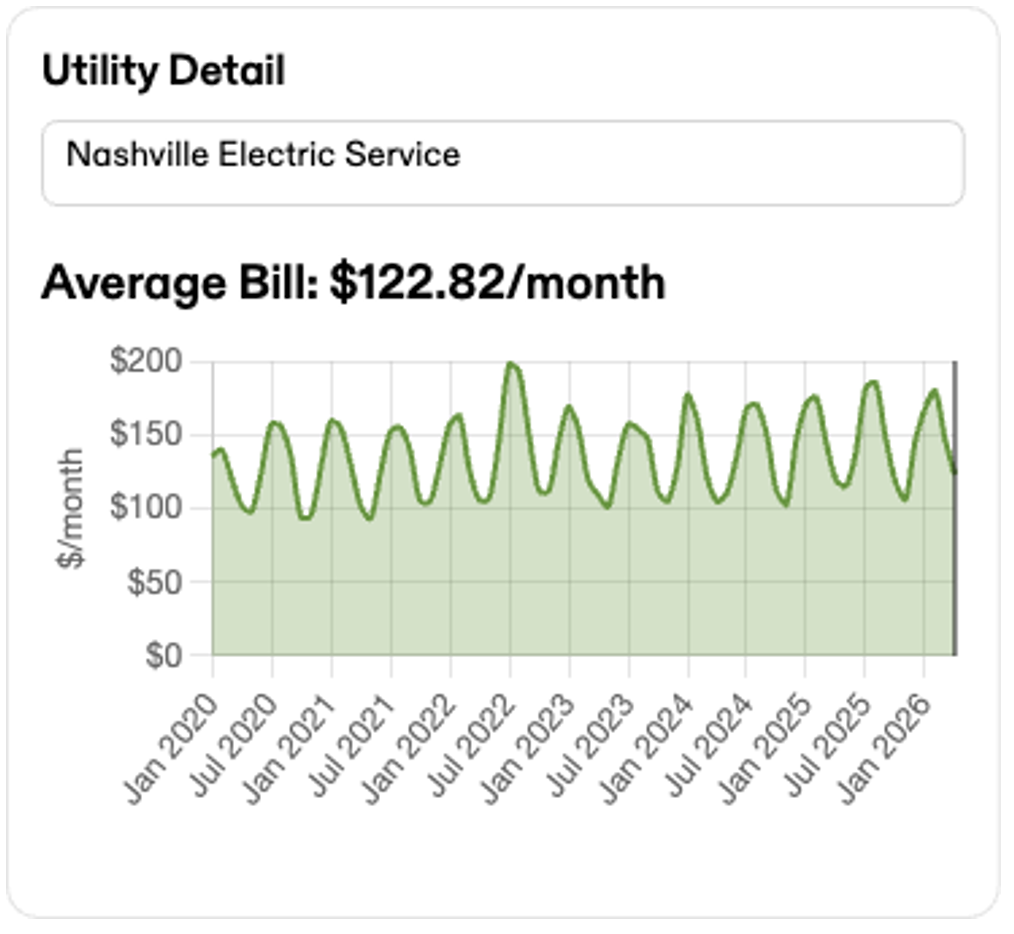

Nashville Electric Service (NES) — one of the eleven largest public electric utilities in the United States — distributes power to all of Davidson County and portions of six surrounding counties, sourcing its supply from the Tennessee Valley Authority (TVA). TVA is the largest public power provider in the country and the backbone of the region’s energy infrastructure.

Data center demand across TVA’s service area reached 18% of total industrial load in 2025, and TVA’s president and CEO has stated publicly that the authority projects data center demand to double within its footprint by 2030. To meet this demand, TVA has launched what it describes as the largest capital program in its history: 6.2 GW of new generation, with 3.7 GW already under active construction. This includes new gas plants replacing coal assets — a significant grid modernization investment.

Davidson County’s commercial electricity rates run approximately 3.2% above the Tennessee state average but 33.5% below the national average — a meaningful structural cost advantage. TVA has also pledged to address “electric rate fairness” to ensure data center load growth does not shift costs onto residential ratepayers, which distinguishes the TVA/NES model from the utility situations in Phoenix and Atlanta where cost-shifting debates are more acute.

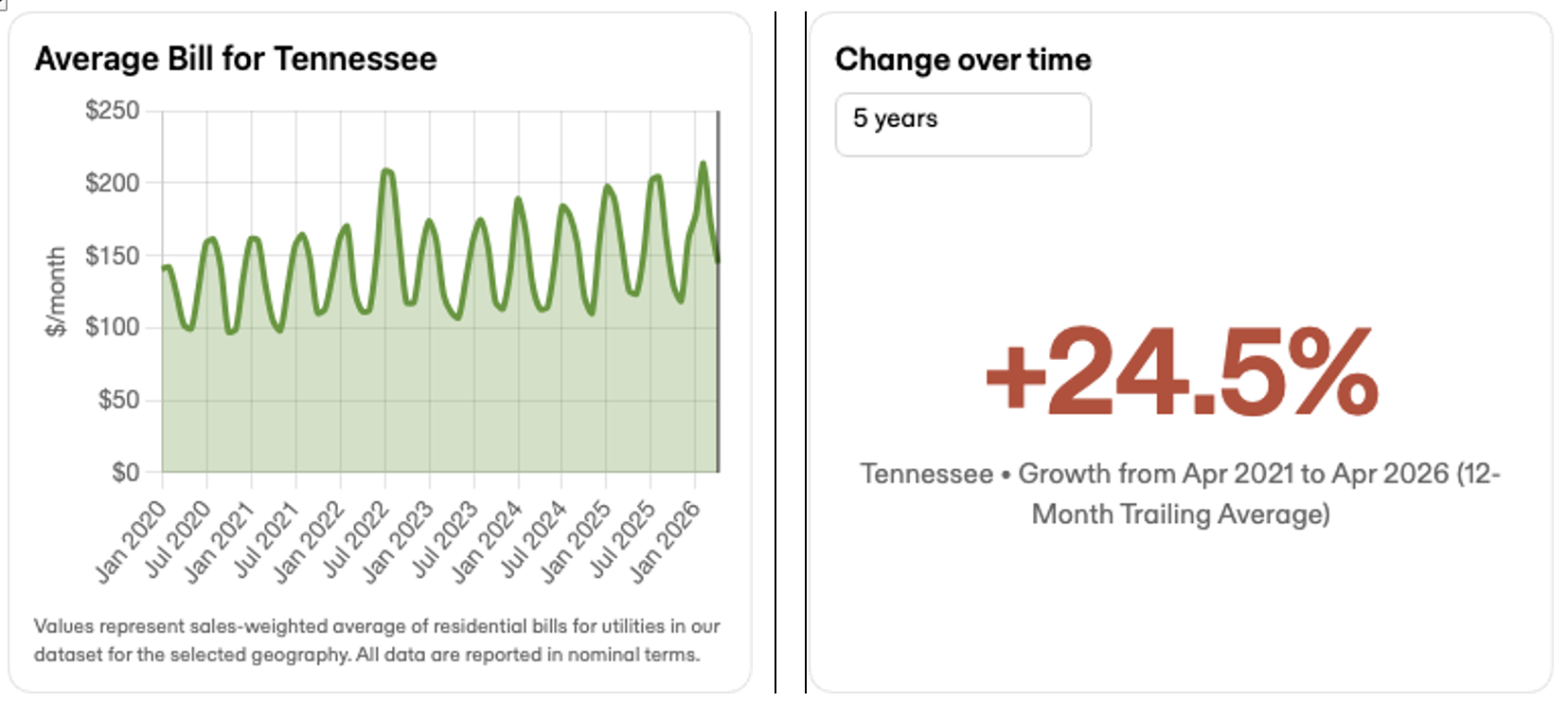

The charts below illustrate electricity cost trends for Tennessee (Nashville Electric Service area). Average bills have increased +24.5% over the five years ending April 2026 — moderate relative to Phoenix (+33.8%) and Miami (+33.8%), reflecting TVA’s position as a large, publicly accountable utility with long-term rate stability as a stated priority.

Nashville Electric Service (NES) utility cost breakdown (generation, transmission, distribution):

Davidson County has no data center moratorium and no restrictive ordinances of the type seen in Denver or Atlanta’s suburban markets. The risk report for Davidson County shows no restrictive ordinances or moratoriums at the county level — a genuinely clean regulatory environment. One contested project (Nashville I) appears in the database, reflecting community engagement during the development process rather than organized opposition that blocked or delayed the facility; Nashville I opened on schedule in 2026.

At the state level, Tennessee lawmakers introduced seven data center bills in 2026, but only one crossed the legislative finish line: a bill giving large data centers the ability to self-power with limited regulation — a pro-development outcome that further strengthens Tennessee’s position as a data center-friendly state.

The environmental profile is favorable compared to most markets in this series. Davidson County carries a very low drought risk, Low water depletion, Low-Medium water stress — among the best water profiles of any Radius DC market. Annual precipitation of 51.9 inches is well above the national average. Protected land coverage is only 11% — below average — with no critical habitat observed in the county.

Nashville’s data center case is straightforward and improving:

Jaymie Scotto & Associates (JSA)

.png)