Platform

Locations

Insights and Resources

News

About

Connect

XThis report provides market context for organizations evaluating Phoenix and the broader Maricopa County area as a location for data center operations. It covers supply and demand dynamics, connectivity infrastructure, the regulatory and power environment, and tax incentives — drawing on current third-party research, local reporting, and publicly available market data.

Phoenix has emerged as one of the most significant data center markets in the United States. As of mid-2025, the metro ranked fourth in total inventory among North American primary markets, having surpassed Silicon Valley for the first time, with 510 MW of total capacity — a 44% year-over-year increase. That trajectory has continued: Maricopa County now hosts at least 2,381 MW of operating data center capacity with a further 2,978 MW planned or under construction, placing Phoenix second nationally in development pipeline behind only Northern Virginia.

The driving forces are well established: favorable climate, competitive land costs, a business-friendly regulatory history, and proximity to major West Coast enterprise and technology markets. AI-driven demand has amplified all of these factors. JLL's Midyear 2025 report placed the Phoenix metro vacancy rate at just 3% — with most major deliveries scheduled for early 2026 already pre-leased. The practical consequence for buyers is that committing ahead of delivery has become the market norm rather than the exception.

One important distinction: growth in Phoenix is increasingly bifurcated. Hyperscale and large-wholesale demand is migrating to outer submarkets — Avondale, Buckeye, Goodyear, Mesa — where campus-scale acreage is available. Network-dense, carrier-rich colocation in the urban core serves a fundamentally different set of requirements and operates in a tighter, more constrained availability environment.

Phoenix sits at the intersection of several major transcontinental fiber routes and has developed a deep carrier ecosystem over the past two decades. The market benefits from diverse long-haul fiber connecting it to Los Angeles, Dallas, Denver, and the broader Southwest — making it a logical aggregation and peering point for traffic serving the western United States.

For enterprise and network operator deployments, access to a carrier-neutral facility with multiple physical points of entry and an active meet-me room is critical. Phoenix’s colocation market has historically offered this through its downtown and Tempe/University corridor facilities, which remain the hub of the market’s interconnection ecosystem.

The distinction between network-dense facilities in the urban core and the newer large-format campuses in the outer submarkets is meaningful for buyers with latency, peering, or carrier diversity requirements: not all Phoenix capacity is equivalently connected.

Phoenix hosts a broad mix of operators across the full spectrum of deployment types. The urban core and Tempe corridor are anchored by network-dense colocation providers — including Radius DC at 3402 E University Drive — that serve enterprise, network, and carrier requirements. The broader metro is served by large-scale wholesale operators with campus developments across Mesa, Avondale, Goodyear, and the outer West Valley.

Activity in the pipeline is substantial. CBRE’s H2 2025 data shows 256 MW absorbed across four citywide projects in H2 2025 alone, with full-scale completions in Mesa, Phoenix, Avondale, Goodyear, and Glendale expected within the following 12 months. Notable recent developments include a new zero-water cooling facility in Mesa delivered in April 2026, and Prime Data Centers breaking ground on a multi-building campus in May 2026. Longer-horizon projects, including a 2.25 million sq ft, nine-building campus proposed near Tonopah approved by Maricopa County in February 2026, signal the scale of long-range interest in the region.

Key takeaway: Phoenix has substantial new supply entering the market — but the majority is large-format and hyperscale-oriented. Carrier-neutral, network-dense colocation in the urban core remains the scarce product, and available inventory in that segment is being absorbed quickly.

Power has become the single most important variable in the Phoenix data center market. Arizona Public Service (APS), the largest electric utility in the state, has publicly acknowledged it is turning away new data center customers due to insufficient generation and transmission capacity. APS currently serves approximately 350 MW of data center load; if every pending applicant were connected, that figure would reach 19,000 MW against peak system capacity of approximately 8,200 MW. APS’s data center strategy director has stated plainly: “We can serve you, but just not now.”

Salt River Project (SRP), the other primary utility serving the metro, is processing its first cluster study of 25 data center applicants — with mixed initial results. SRP is also adding 12 new natural gas turbines to support grid capacity. Average time to power for new energy projects in Maricopa County currently runs approximately 4 years 6 months, well above the state average of 4.3 years. For buyers requiring new power interconnections, this timeline is a material planning variable.

The critical implication for colocation buyers: facilities with existing, contracted power capacity represent meaningfully different value than sites requiring new interconnections. An established colocation facility with allocated utility capacity sidesteps the interconnection queue entirely.

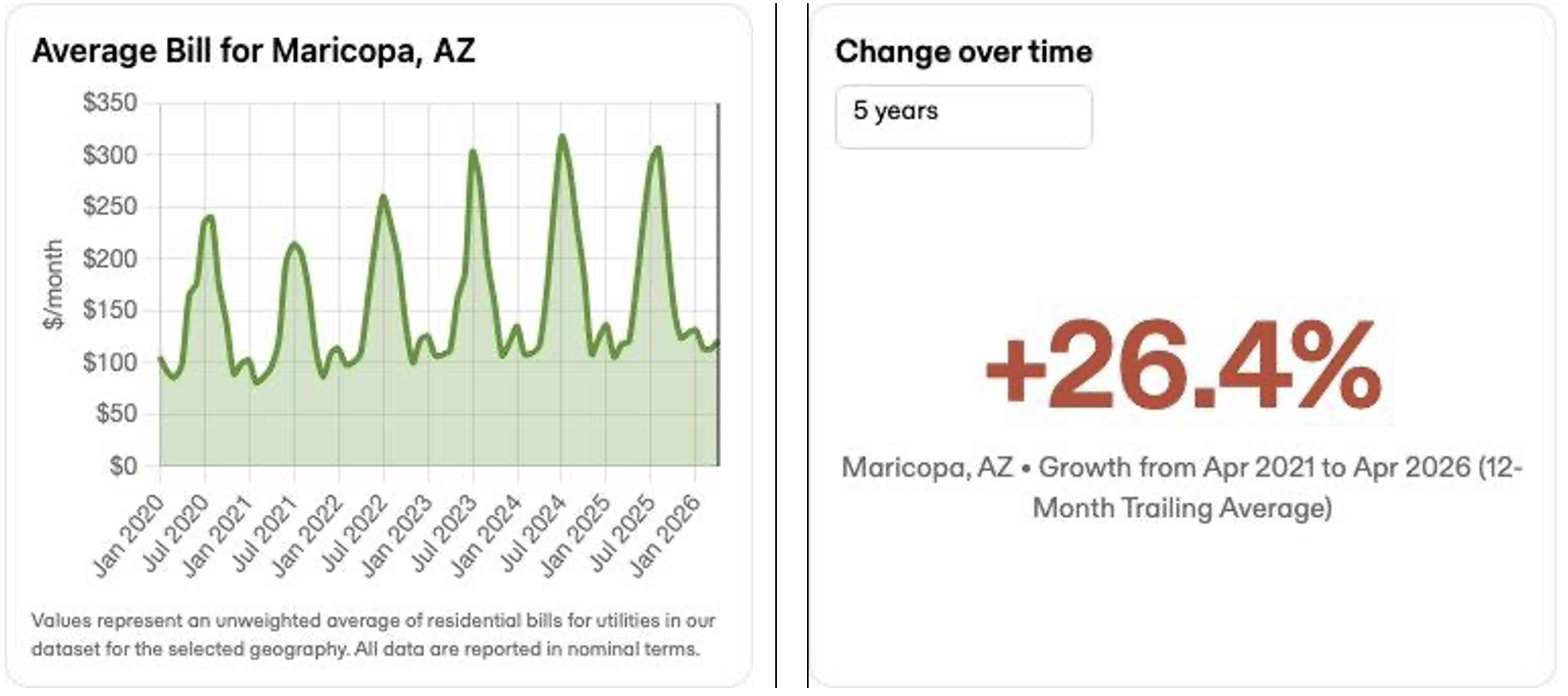

The charts below illustrate electricity cost trends for the Phoenix metro. Average residential bills in Maricopa County have risen 26.4% over the five years ending April 2026, driven by a combination of population growth, extreme summer demand peaks, and the cost of grid expansion. APS bills reflect strong seasonality, with summer cooling loads pushing bills significantly above the annual average.

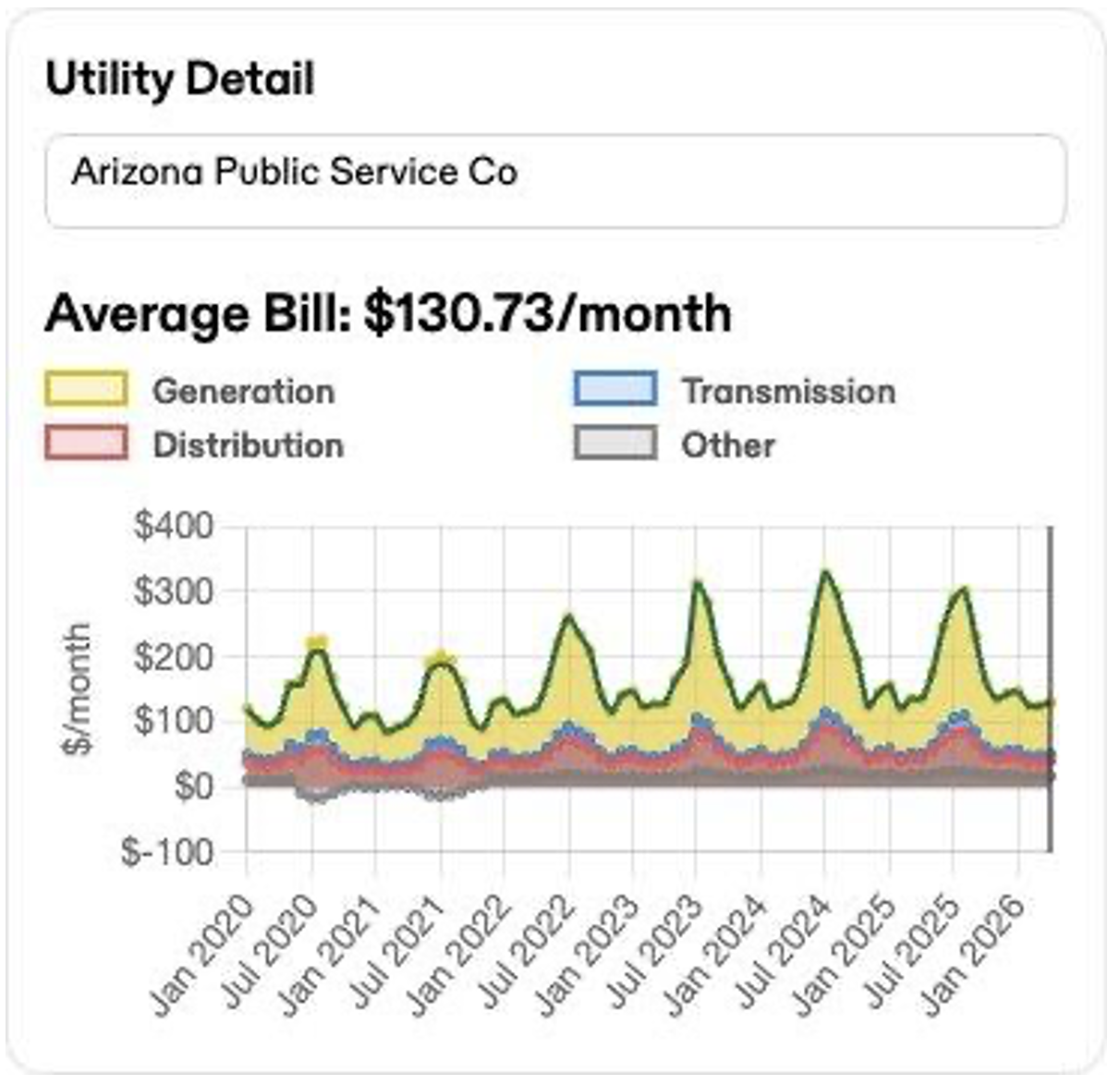

APS utility cost breakdown (generation, transmission, distribution):

Arizona has historically offered one of the most attractive tax incentive packages for data center investment in the United States. The state’s Computer Data Center Program, administered by the Arizona Commerce Authority, provides Transaction Privilege Tax (TPT) and Use Tax exemptions at the state, county, and local levels on qualifying equipment purchases. For facilities in Maricopa County, the minimum qualifying investment threshold is $50 million; exemptions are available for 10 years from certification, or up to 20 years for projects qualifying as Sustainable Redevelopment Projects. The program is currently authorized through December 31, 2033.

However, the incentive is under active political scrutiny. Governor Katie Hobbs called for its repeal in her January 2026 State of the State address, and the Arizona Legislature is weighing legislation to sunset the exemption. The program cost the state an estimated $38.5 million in fiscal year 2025, a figure projected to grow to at least $60 million by FY2027. The outcome of this legislative debate will be an important variable for organizations with long-term Arizona cost models that include TPT savings.

For colocation tenants, the TPT exemption can apply to qualifying equipment purchases — making it worth evaluating with your tax and legal advisors against your specific deployment structure.

The regulatory posture toward data centers in Phoenix has shifted materially since 2024. In July 2025, the city of Phoenix imposed new data center regulations citing concerns over power and water demand, and several proposed projects were rejected or canceled. Phoenix Mayor Kate Gallego publicly criticized data centers in a May 2025 State of the City address, citing energy demand, water use, and neighborhood impact.

At the county level, Maricopa County continues to approve large-scale projects in unincorporated areas, as evidenced by the February 2026 approval of a nine-building campus near Tonopah. The regulatory picture is therefore submarket-dependent: city of Phoenix is restrictive for new development, while outer county jurisdictions remain more accommodating for large-format projects.

Water is a recurring concern across the region. Both APS and SRP service territory cities require new industrial water users to limit consumption, and in some cases, large users must secure independent water supplies. Operators like Edged Energy have responded by building zero-water evaporative cooling systems — a direction the market is likely to continue to reward as water policy tightens. Notably, Maricopa County’s drought risk is classified as “Relatively Moderate” with high water stress and depletion levels — a manageable but real constraint on development.

What this means for buyers: Established facilities with existing operating permits, contracted power, and water compliance are not subject to the new restrictions being placed on development applicants. The regulatory environment differentiates existing inventory from new development — another reason near-term buyers should focus on currently operational facilities.

Despite emerging constraints, Phoenix’s fundamental market attributes remain compelling:

Jaymie Scotto & Associates (JSA)

.png)